🕔 Modelling and Predicting Time Series

In this module we will look at modelling of time series. We will start with the simplest of exponential models and go all the way through ARIMA and forecasting with Prophet.

First, some terminology!

Additive Time Series can be represented as:

Multiplicative Time Series can be described as:

Let us consider a Multiplicative Time Series, pertaining to sales of souvenirs at beaches in Australia: The time series looks like this:

Note that along with the trend, the amplitude of both seasonal and noise components are also increasing in a multiplicative way here !! A multiplicative time series can be converted to additive by taking a log of the time series.

Stationarity

A time series is said to be stationary if it holds the following conditions true:

- The mean value of time-series is constant over time, which implies, the trend component is nullified/constant.

- The variance does not increase over time.

- Seasonality effect is minimal.

This means it is devoid of trend or seasonal patterns, which makes it looks like a random white noise irrespective of the observed time interval , i.e. zooming in on the time axis. ( i.e. self-similar and fractal)

A Bit of Forecasting?

We are always interested in the future. We will do this in three ways:

- use Simple Exponential Smoothing

- use a package called

forecastto fit an ARIMA (Autoregressive Moving Average Integrated Model) model to the data and make predictions for weekly sales; - And do the same using a package called

prophet.

Forecasting using Exponential Smoothing

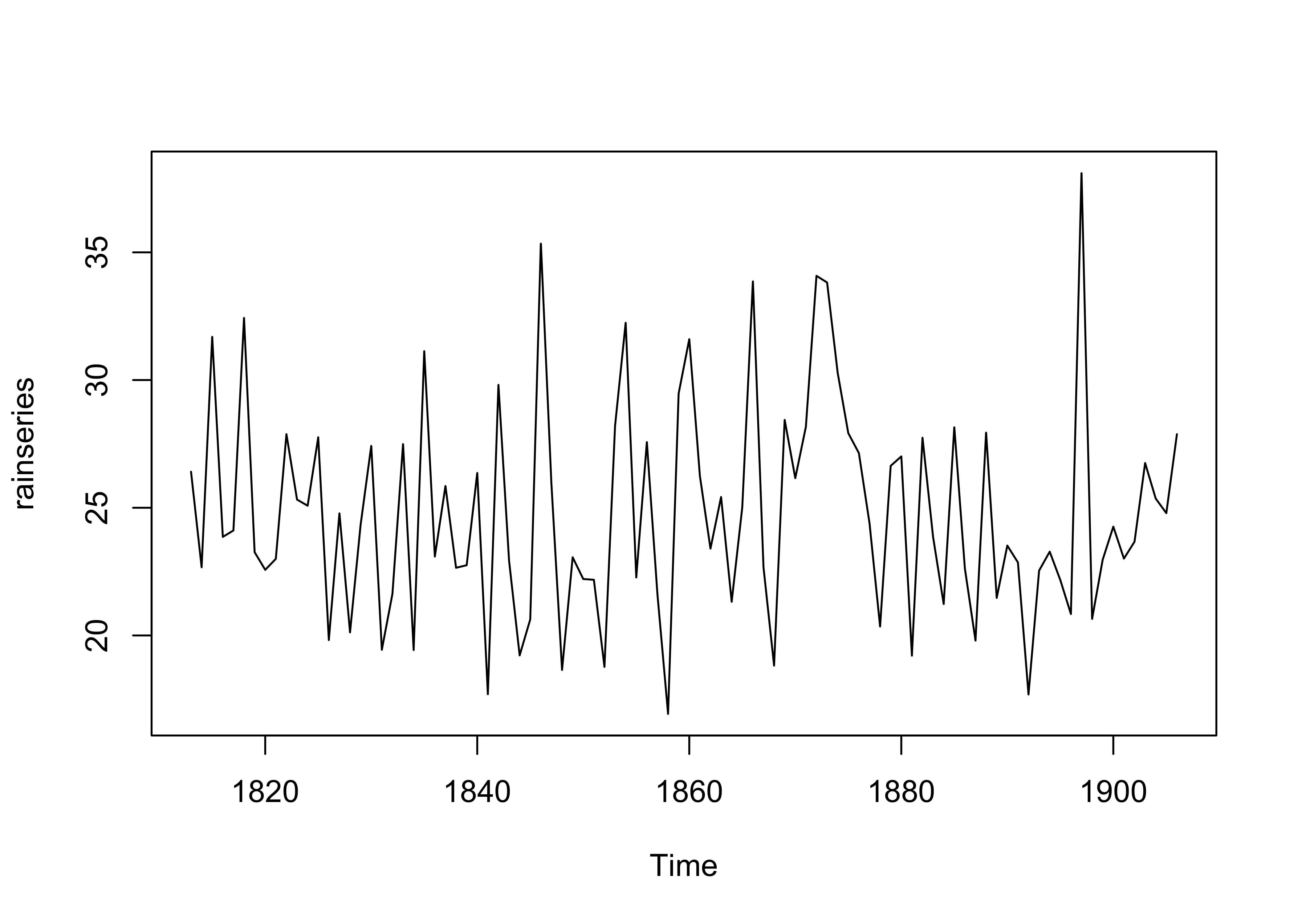

For example, the file contains total annual rainfall in inches for London, from 1813-1912 (original data from Hipel and McLeod, 1994).

rain <- scan("https://robjhyndman.com/tsdldata/hurst/precip1.dat", skip = 2)

rainseries <- ts(rain, start = c(1813))

plot(rainseries)

There is a nearly constant value of about 25 around which there are random fluctuations and it seems to be an additive model. How can we make forecasts with this time series?

A deliberate detour:

Let’s see some quick notation to aid understanding: Much of smoothing is based on the high school concept of a straight line,

In the following, we choose to describe the models with:

-

-

-

-

-

In Exponential Smoothing and Forecasting, we make three models of increasing complexity:

Simple Exponential Model: Here we deal only with the mean or level aspect of the (decomposed) time series and make predictions with that.

Holt Model: Here we use the

leveland thetrendfrom the decomposed time series for predictionsHolt-Winters Model: Here we use the

level, thetrend, and theseasonalcomponent from the decomposed time series for predictions.

[<start>st]->[<input>input]

[<input> input]->[<package> Time Series|Decomposition]

[<package> Time Series|Decomposition]->[<component> Mean/Level]

[<package> Time Series|Decomposition]->[<component> Slope/Trend]

[<package> Time Series|Decomposition]->[<component> Seasonal]

//Simple Exponential Smoothing

[<component> Mean/Level]->[Delay A1]

[Delay A1]->[Delay A2]

[Delay A2]->[Delay A3]

[Delay A3]...->...[Delay AN]

[Delay A1]->[<state> A1]

[Delay A2]->[<state> A2]

[Delay A3]->[<state> A3]

[Delay AN]->[<state> AN]

[<state> AN]---([<note> $$alpha(1-alpha)^i$$]

[<state> A1]->[<state> Add1]

[<state> A2]->[<state> Add1]

[<state> A3]->[<state> Add1]

[<state> AN]->[<state> Add1]

[<state> Add1]->[<end> Output]

//Holt

[<component> Slope/Trend]->[Delay B1]

[Delay B1]->[Delay B2]

[Delay B2]->[Delay B3]

[Delay B3]...->...[Delay BN]

[Delay B1]->[<state> B1]

[Delay B2]->[<state> B2]

[Delay B3]->[<state> B3]

[Delay BN]->[<state> BN]

[<state> BN]---([<note> $$beta(1-beta)^i$$]

[<state> B1]->[<state> Add2]

[<state> B2]->[<state> Add2]

[<state> B3]->[<state> Add2]

[<state> BN]->[<state> Add2]

[<state> Add2]->[<end> Output]

// Holt Winters

[<component> Seasonal]->[Delay C1]

[Delay C1]->[Delay C2]

[Delay C2]->[Delay C3]

[Delay C3]...->...[Delay CN]

[Delay C1]->[<state> C1]

[Delay C2]->[<state> C2]

[Delay C3]->[<state> C3]

[Delay CN]->[<state> CN]

[<state> CN]---([<note> $$gamma(1-gamma)^i$$]

[<state> C1]->[<state> Add3]

[<state> C2]->[<state> Add3]

[<state> C3]->[<state> Add3]

[<state> CN]->[<state> Add3]

[<state> Add3]->[<end> Output]

// Final Output

[<end> Output]->[<receiver> Forecast]Simple Smoothing is smoothing based forecasting using just the level ( i.e. mean) of the Time Series to make forecasts.

Double exponential smoothing, or Holt Smoothing Model, is just exponential smoothing applied to both level and trend.

The idea behind triple exponential smoothing, or the Holt-Winters Smoothing Model, is to apply exponential smoothing to the seasonal components in addition to level and trend.

What does “Exponential” mean?

All three models use memory: at each time instant in the Time Series, a set of past values, along with the present sample is used to make a prediction of the relevant parameter ( level / slope / seasonal). These are then added together to make the forecast.

The memory in each case controlled by a parameter: alpha for the estimate of the level beta for the slope estimate, and gamma for the seasonal component estimate at the current time point. All these parameters are between 0 and 1. The model takes a weighted average of past values of each parameter. The weights are derived in the form of

To make forecasts using simple exponential smoothing in R, we can use the HoltWinters() function in R, or the forecast::ets() function from forecasts. This latter function is more powerful.

args(HoltWinters)function (x, alpha = NULL, beta = NULL, gamma = NULL, seasonal = c("additive",

"multiplicative"), start.periods = 2, l.start = NULL, b.start = NULL,

s.start = NULL, optim.start = c(alpha = 0.3, beta = 0.1,

gamma = 0.1), optim.control = list())

NULLfunction (y, model = "ZZZ", damped = NULL, alpha = NULL, beta = NULL,

gamma = NULL, phi = NULL, additive.only = FALSE, lambda = NULL,

biasadj = FALSE, lower = c(rep(1e-04, 3), 0.8), upper = c(rep(0.9999,

3), 0.98), opt.crit = c("lik", "amse", "mse", "sigma",

"mae"), nmse = 3, bounds = c("both", "usual", "admissible"),

ic = c("aicc", "aic", "bic"), restrict = TRUE, allow.multiplicative.trend = FALSE,

use.initial.values = FALSE, na.action = c("na.contiguous",

"na.interp", "na.fail"), ...)

NULLTo use HoltWinters() for simple exponential smoothing, we need to set the parameters beta=FALSE and gamma=FALSE in the HoltWinters() function (the beta and gamma parameters are used for double exponential smoothing, or triple exponential smoothing.

To use forecast::ets, we set the model argument to “ANN”, “AAN”, and “AAA” respectively for each of the three smoothing models.

Note: The HoltWinters() function returns a list variable, that contains several named elements.

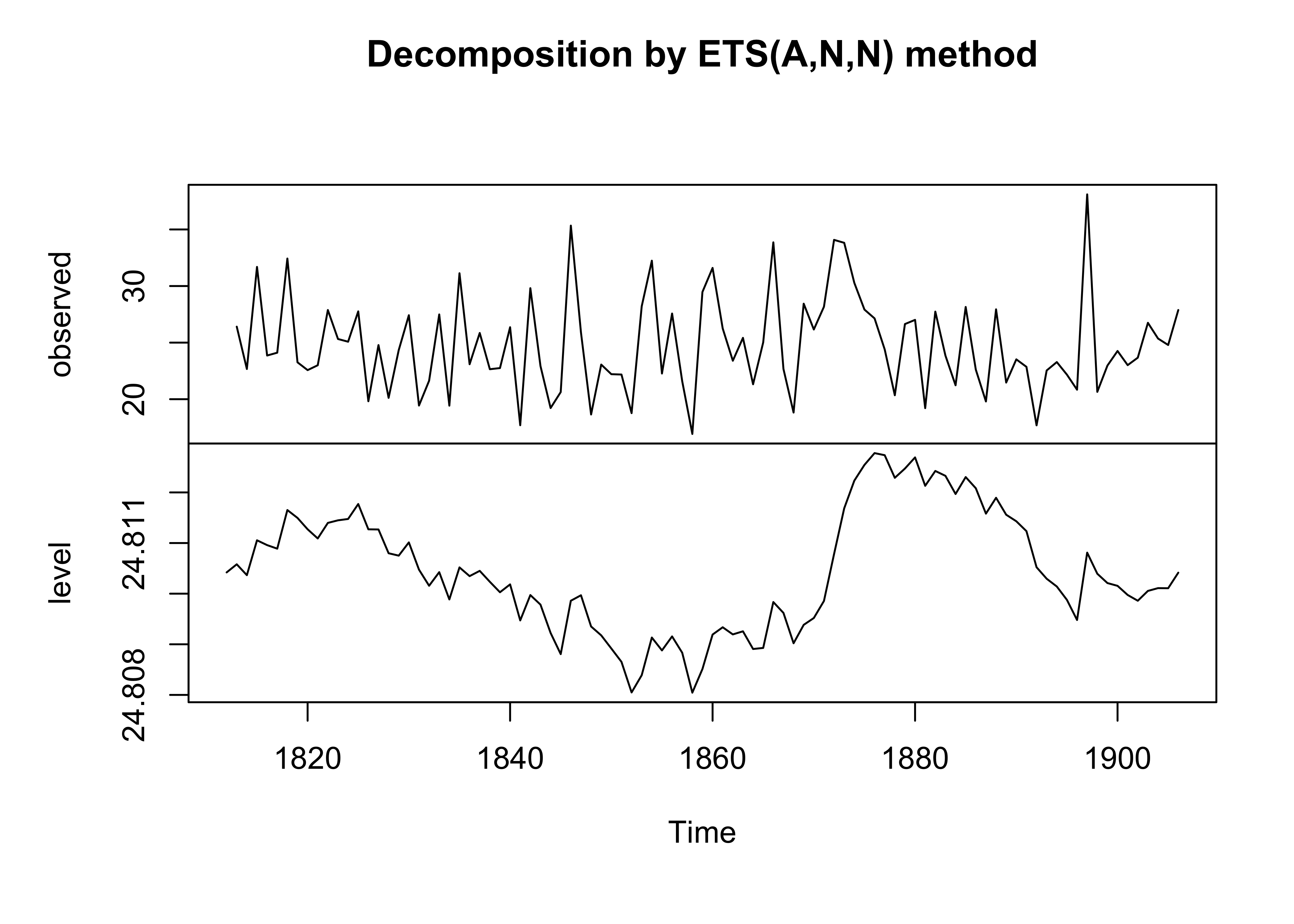

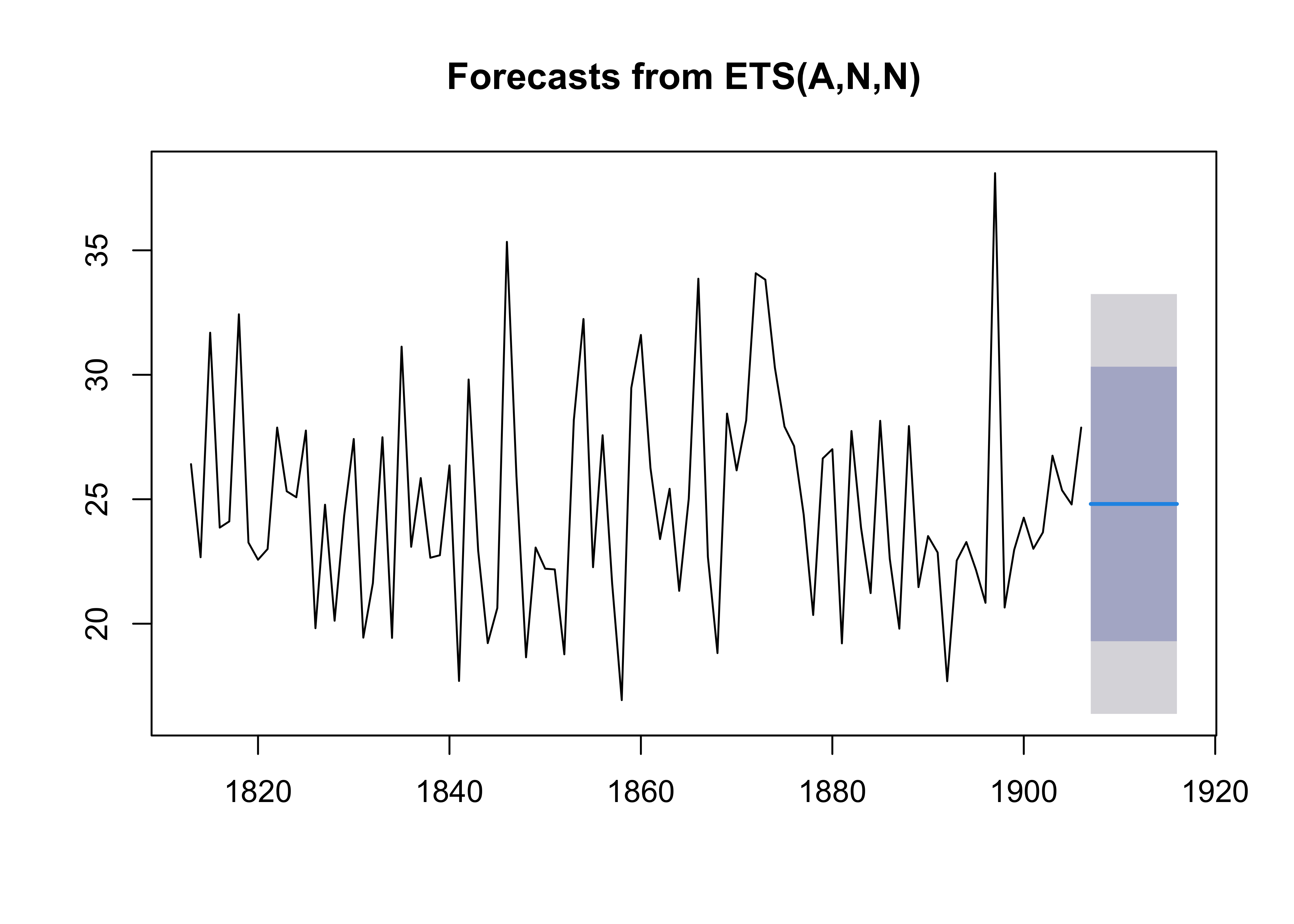

rainseriesforecasts <- forecast::ets(rainseries, model = "ANN")

# class(rainseriesforecasts)

# str(rainseriesforecasts)

plot(rainseriesforecasts)

ARIMA

We can also use past trends and seasonality in the data to make predictions about the future using the forecast package. Here we use an auto ARIMA model to guess at the trend in the time series. Then we use that model to forecast a few periods into the future.

Mathematically an ARIMA model can be shown as follows:

We will use the familiar Walmart Sales dataset, and try to predict weekly sales for one of the Departments.

data("walmart_sales_weekly")

walmart_wide <- walmart_sales_weekly %>%

pivot_wider(.,

id_cols = c(Date),

names_from = Dept,

values_from = Weekly_Sales,

names_prefix = "Sales_"

)

## forecast::auto.arima needs a SINGLE time series, so we pick one, Dept95

sales_95_ts <- walmart_wide %>%

select(Sales_95) %>%

ts(start = c(2010, 1), end = c(2012, 52), frequency = 52)

sales_95_tsTime Series:

Start = c(2010, 1)

End = c(2012, 52)

Frequency = 52

[1] 106690.06 111390.36 107952.07 103652.58 112807.75 112048.41 117716.13

[8] 113117.35 111466.37 116770.82 126341.84 110204.77 107648.14 125592.28

[15] 120247.90 120036.99 121902.19 133056.97 131995.00 134118.05 120172.47

[22] 124821.44 126241.20 121386.73 116256.35 108781.57 131128.96 131288.83

[29] 124601.48 117929.58 124220.10 125027.49 124372.90 114702.69 113009.41

[36] 120764.22 123510.99 110052.15 105793.40 110332.92 110209.31 107544.02

[43] 106015.41 100834.31 111384.36 116521.67 121695.13 93676.95 107317.32

[50] 109955.90 103724.16 99043.34 114270.08 117548.75 112165.80 107742.95

[57] 116225.68 120621.32 123405.41 122280.13 112905.09 126746.25 126834.30

[64] 118632.26 111764.31 120882.84 124953.94 112581.20 119815.67 135260.49

[71] 136364.46 135197.63 121814.84 128054.88 133213.04 127906.50 121483.11

[78] 117284.94 138538.47 138567.10 133260.84 122721.92 130446.34 133762.77

[85] 133939.40 116165.28 115663.78 132805.42 125954.30 116931.34 108018.21

[92] 114793.92 115047.16 113966.34 112688.97 102798.99 119053.80 120721.07

[99] 125041.39 93358.91 116427.93 118685.12 113021.23 102202.04 115507.25

[106] 125038.09 119807.63 110870.94 118406.27 125840.82 132318.50 117030.73

[113] 127706.00 137958.76 129438.22 123172.79 118589.44 130920.36 131341.85

[120] 129031.19 127603.00 130573.37 139857.10 140806.36 124594.40 131935.56

[127] 148798.05 129724.74 126861.49 121030.79 134832.22 137408.20 136264.68

[134] 118845.34 124741.33 140657.40 128542.73 119121.35 115326.47 127009.22

[141] 124559.93 123346.24 117375.38 106690.06 111390.36 107952.07 103652.58

[148] 112807.75 112048.41 117716.13 113117.35 111466.37 116770.82 126341.84

[155] 110204.77 107648.14arima_dept_95 <- forecast::auto.arima(y = sales_95_ts)

arima_dept_95Series: sales_95_ts

ARIMA(0,1,1)(0,1,0)[52]

Coefficients:

ma1

-0.8842

s.e. 0.0530

sigma^2 = 29974424: log likelihood = -1033.02

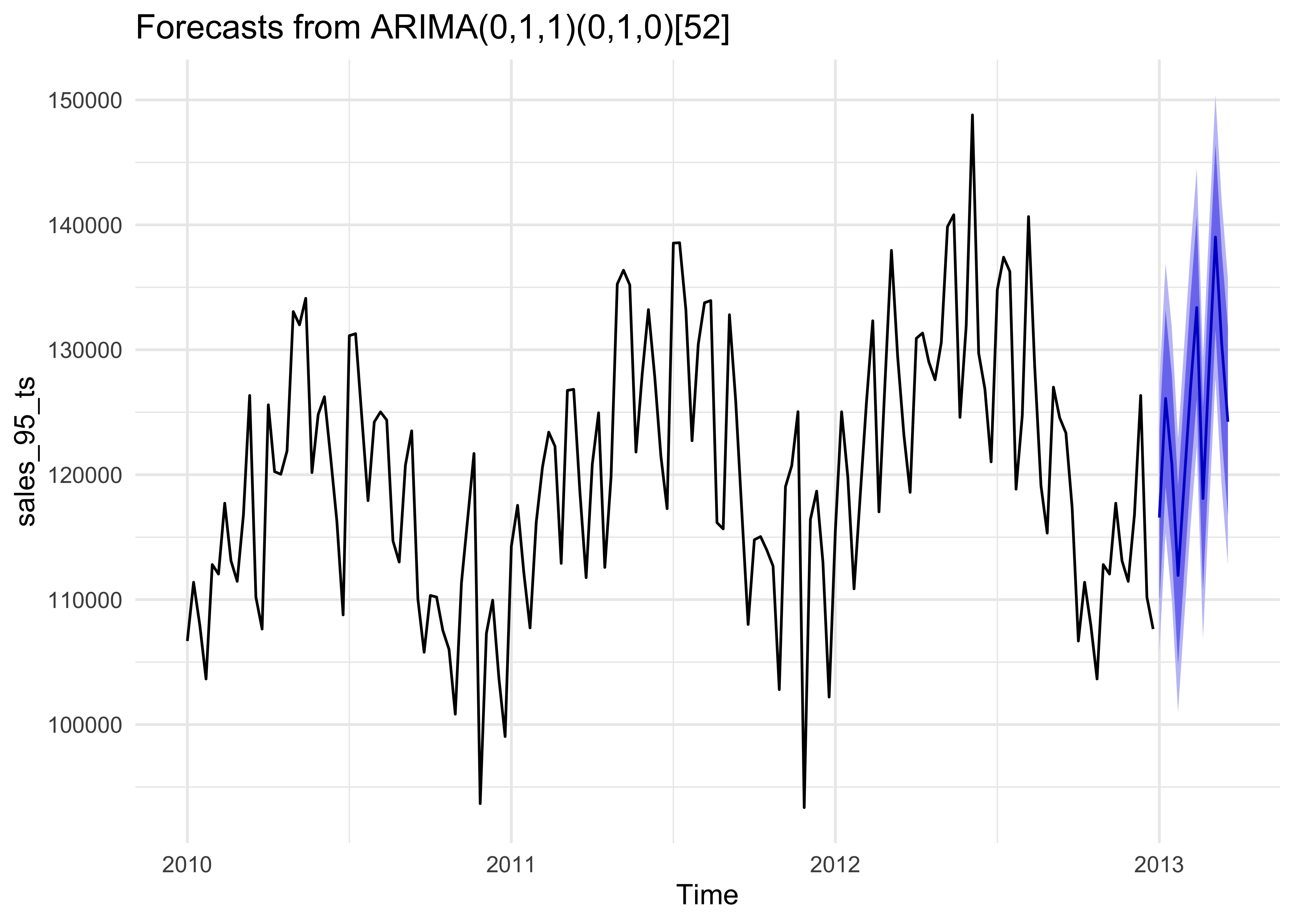

AIC=2070.03 AICc=2070.15 BIC=2075.3plot(arima_dept_95)

# Use the model to forecast 12 weeks into the future

sales95_forecast <- forecast(arima_dept_95, h = 12)

# Plot the forecast. Again, we can use autoplot.

autoplot(sales95_forecast) +

theme_minimal()

We’re fairly limited in what we can actually tweak when using autoplot(), so instead we can convert the forecast object to a data frame and use ggplot() like normal:

# Get data out of this weird sales95_forecast object

sales95_forecast Point Forecast Lo 80 Hi 80 Lo 95 Hi 95

2013.000 116571.1 109554.8 123587.5 105840.6 127301.7

2013.019 126102.0 119038.7 133165.2 115299.7 136904.3

2013.038 120871.5 113761.7 127981.4 109998.0 131745.1

2013.058 111934.8 104778.7 119091.0 100990.5 122879.2

2013.077 119470.2 112268.0 126672.3 108455.5 130484.9

2013.096 126904.7 119656.9 134152.5 115820.1 137989.3

2013.115 133382.4 126089.2 140675.6 122228.3 144536.5

2013.135 118094.6 110756.3 125433.0 106871.6 129317.7

2013.154 128769.9 121386.7 136153.1 117478.2 140061.6

2013.173 139022.7 131594.8 146450.5 127662.8 150382.5

2013.192 130502.1 123030.0 137974.3 119074.5 141929.8

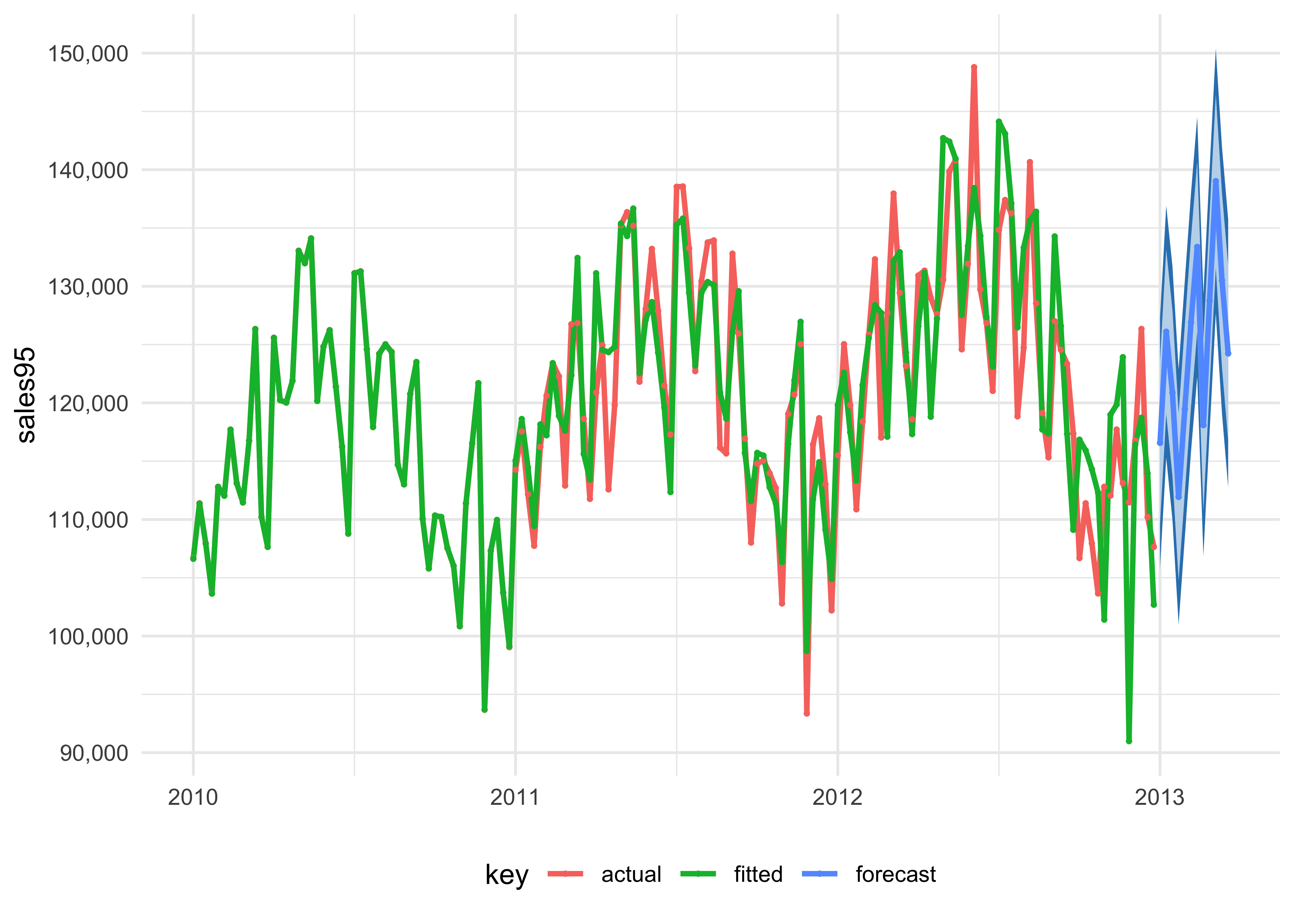

2013.212 124236.7 116720.5 131752.9 112741.7 135731.7sales95_forecast_tidy <- sweep::sw_sweep(sales95_forecast,

fitted = TRUE,

timetk_idx = TRUE

)

sales95_forecast_tidyindex <dbl> | key <chr> | value <dbl> | lo.80 <dbl> | lo.95 <dbl> | hi.80 <dbl> | hi.95 <dbl> |

|---|---|---|---|---|---|---|

| 2010.000 | actual | 106690.06 | NA | NA | NA | NA |

| 2010.019 | actual | 111390.36 | NA | NA | NA | NA |

| 2010.038 | actual | 107952.07 | NA | NA | NA | NA |

| 2010.058 | actual | 103652.58 | NA | NA | NA | NA |

| 2010.077 | actual | 112807.75 | NA | NA | NA | NA |

| 2010.096 | actual | 112048.41 | NA | NA | NA | NA |

| 2010.115 | actual | 117716.13 | NA | NA | NA | NA |

| 2010.135 | actual | 113117.35 | NA | NA | NA | NA |

| 2010.154 | actual | 111466.37 | NA | NA | NA | NA |

| 2010.173 | actual | 116770.82 | NA | NA | NA | NA |

# For whatever reason, the date column here is a special type of variable called

# "yearmon", which ggplot doesn't know how to deal with (like, we can't zoom in

# on the plot with coord_cartesian). We use zoo::as.Date() to convert the

# yearmon variable into a regular date

sales95_forecast_tidy_real_date <-

sales95_forecast_tidy %>%

mutate(actual_date = zoo::as.Date(index, frac = 1))

sales95_forecast_tidy_real_dateindex <dbl> | key <chr> | value <dbl> | lo.80 <dbl> | lo.95 <dbl> | hi.80 <dbl> | hi.95 <dbl> | actual_date <date> |

|---|---|---|---|---|---|---|---|

| 2010.000 | actual | 106690.06 | NA | NA | NA | NA | 1975-07-04 |

| 2010.019 | actual | 111390.36 | NA | NA | NA | NA | 1975-07-04 |

| 2010.038 | actual | 107952.07 | NA | NA | NA | NA | 1975-07-04 |

| 2010.058 | actual | 103652.58 | NA | NA | NA | NA | 1975-07-04 |

| 2010.077 | actual | 112807.75 | NA | NA | NA | NA | 1975-07-04 |

| 2010.096 | actual | 112048.41 | NA | NA | NA | NA | 1975-07-04 |

| 2010.115 | actual | 117716.13 | NA | NA | NA | NA | 1975-07-04 |

| 2010.135 | actual | 113117.35 | NA | NA | NA | NA | 1975-07-04 |

| 2010.154 | actual | 111466.37 | NA | NA | NA | NA | 1975-07-04 |

| 2010.173 | actual | 116770.82 | NA | NA | NA | NA | 1975-07-04 |

# Plot this puppy!

ggplot(sales95_forecast_tidy, aes(x = index, y = value, color = key)) +

geom_ribbon(aes(ymin = lo.95, ymax = hi.95),

fill = "#3182bd", color = NA

) +

geom_ribbon(aes(ymin = lo.80, ymax = hi.80, fill = key),

fill = "#deebf7", color = NA, alpha = 0.8

) +

geom_line(size = 1) +

geom_point(size = 0.5) +

labs(x = NULL, y = "sales95") +

scale_y_continuous(labels = scales::comma) +

# Zoom in on 2012-2016

# coord_cartesian(xlim = ymd(c("2004-07-01", "2007-07-31"))) +

theme_minimal() +

theme(legend.position = "bottom")

plot_time_series(.data = sales95_forecast_tidy, .date_var = index, .value = value, .color_var = key, .smooth = FALSE)A Bit of Forecasting?

We are always interested in the future. We will do this in three ways:

- use Simple Exponential Smoothing

- use a package called

forecastto fit an ARIMA (Auto-regressive Moving Average Integrated Model) model to the data and make predictions for weekly sales; - And do the same using a package called ’prophet`.

Conclusion

References

1, Shampoo Dataset Brownlee: https://raw.githubusercontent.com/jbrownlee/Datasets/master/shampoo.csv